Key data for the 2014 financial year of the Dillinger Hütte Group

15 April 2015

Despite highly problematic market conditions, the Dillinger Hütte Group (Dillinger Hütte and its subsidiaries) was able to increase its production and sales volumes in 2014 compared to the previous year and concluded the financial year with a profit. “The Dillinger Hütte Group has gotten out of the red and has improved its EBIT and EBITDA by more than € 250 million compared to the previous year. This is the result of considerable cost cutting and a significant enhancement of competitiveness,” Dillinger Hütte Chief Executive Officer Dr. Karlheinz Blessing said during the annual press conference.

For instance, savings from the company-wide program DH 2014 plus, at € 145 million, were significantly higher than the planned target of € 130 million. “In the process, we were able to implement all personnel measures in a socially responsible way,” Blessing explained.

Key data

- Dillinger Hütte Group once again clearly in the black

- EBIT improves from a negative € 167 million to a positive € 88 million and EBITDA from a negative € 66 million to a positive € 193 million

- Considerable savings due to cost-cutting and restructuring program DH 2014 plus

- Consolidated revenue increased slightly (+ 1 %) with continued lower revenue levels

However, development of the heavy plate market in 2014 was disappointing. The Asian market was in particular marked by substantial overcapacities. Although average utilization of capacities at European heavy plate steel plants, at almost 70 %, was somewhat higher than the previous year, it was not enough to have a lasting positive impact on the price for heavy plate. Instead, declining raw material costs and a sharp increase in imports from third countries brought intensified price pressures, which caused revenues to fall once again on average in comparison with the previous year.

Figures for the Dillinger Hütte Group for the 2014 financial year:

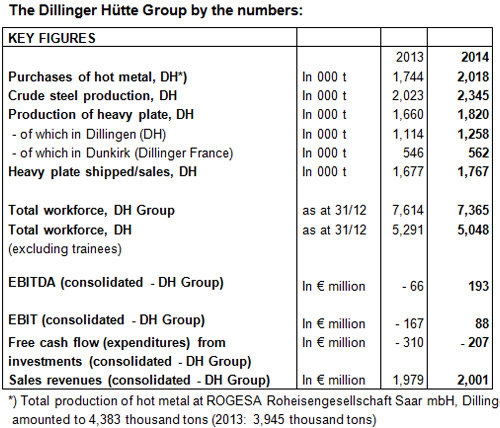

- Production at the rolling mills in Dillingen and in Dunkirk, at the wholly owned subsidiary Dillinger France, rose to 1.820 million tons, compared with 1.660 million tons in 2013.

- Despite low revenue levels, consolidated sales revenue increased slightly due to higher sales volumes, to € 2.001 billion from around € 1.979 billion in the previous year.

- Consolidated earnings before interest and taxes (EBIT) increased from - € 167 million to € 88 million, and consolidated earnings before interest, taxes, depreciation and amortization (EBITDA), rose from - € 66 million to € 193 million.

- At € 207 million, total expenditures for investments (consolidated cash flow from investment activities) for the Dillinger Hütte Group in 2014 continued to be at a high level (previous year:

€ 310 million). - Despite the high investment spending, the equity ratio was 68 % of the balance sheet total.

The focus of investment at Dillinger Hütte itself (€ 140 million) was in the construction of the new CC 6 continuous casting machine, with which the company is securing and further expanding its technological competitive edge. - A total of 5,048 people were employed at the Dillingen location at the end of the financial year (31 Dec 2013: 5,291). These employees worked at Dillinger Hütte itself, at Zentralkokerei Saar GmbH (ZKS), and at ROGESA Roheisengesellschaft Saar mbH (ROGESA). A total of 7,365 people are employed within the Dillinger Hütte Group (2013: 7,614).

- During 2014, 65 young people began vocational training at Dillinger Hütte (2013: 51). As a result, the company employs a total of 206 trainees, when all training class years are included.

Energy policy must not endanger competitiveness

Dillinger Hütte sees the local steel industry as being heavily burdened by German and European energy and climate policies. Dr. Karlheinz Blessing: “It is not the individual components like the EEG surcharge or CO2 emissions trading, but rather the massive accumulation of a wide range of requirements and costs that are progressively suffocating us and putting us at a competitive disadvantage. Added to this is a resulting acceptance of the shifting of production to other steel producing countries outside the EU, which does not benefit the world climate – quite the contrary.”

Weak outlook for 2015 with highly problematic market conditions continuing

Prospects for the heavy plate market remain subdued. Aggressive predatory competition prevails, low gas and oil prices are hampering investment in the energy market, and ongoing overcapacities and high imports are placing intense pressure on prices. A significant increase of the price level for heavy plate will be only partially implementable under these market conditions.

The Dillinger Hütte Group will continue to enhance its competitiveness. In doing so, all efforts are focused on defending and expanding the company’s position as a technology leader in Europe in the fight for market share, without neglecting the interesting niche markets outside of Europe. The strategy program PRIMUS 16 was launched for this purpose in late 2014. It is a package of measures that aims to even better utilize the capacities of production facilities, shorten delivery times, further enhance productivity, and increase flexibility within the company.

In 2015 Dillinger Hütte expects similar overall utilization of production facility capacities in terms of volumes as in 2014, with highly fluctuating quarterly figures. Provided that the cost savings achieved as well as the additional measures to increase profitability as part of the PRIMUS 16 strategy program continue to be effective, the Dillinger Hütte Group expects stable sales volume along with positive earnings figures for 2015 as well, which will be significantly below the previous year’s level.

Pictures of Dillinger Hütte can be found in the download section:

http://www.dillinger.de/dh/aktuelles/info/jpk/index.shtml.de

By using the pictures please pay attention to the different copyrights, as stated in the file name.

Your contacts:

Ute Engel, tel.: +49 (0)6831-473011, email: ute.engel@stahl-holding-saar.de

Ines Oberhofer, tel.: +49 (0)6831-472002, email: ines.oberhofer@stahl-holding-saar.de